Inside Drift: Architecting a High-Performance Orderbook on Solana

Drift Protocol is Solana’s largest open-source perpetual futures DEX, enabling low-slippage, high-leverage trading with cross-margining. It’s crucial for DeFi, handling over $20B in volume since 2021, per CoinGecko.

Architecture of Drift

The architecture of Drift Protocol is built upon the high-performance capabilities of the Solana blockchain, which are essential for supporting a derivatives exchange with features like high leverage and complex order types. Solana’s inherent speed and low transaction costs directly contribute to a smoother and more cost-effective trading experience for users on the Drift platform.

A central element of Drift’s design is its cross-margined risk engine. This system allows users to utilize their entire collateral balance across different assets and positions to meet margin requirements, enhancing capital efficiency. However, this approach necessitates a complex framework for calculating margin and managing potential liquidations across a user’s portfolio. Furthermore, Drift’s orderbook, liquidity provision, and liquidation processes are facilitated by a decentralized Keeper Network. This network, comprised of incentivized agents and market makers, plays a vital role in providing Just-In-Time (JIT) liquidity, executing order matching, and ensuring the timely liquidation of undercollateralized positions.

The architecture revolves around key accounts:

- User Account: Manages individual positions, margins, and collateral.

- PerpMarket Account: Stores market data, including pricing and liquidity for perpetuals.

- State Account: Holds global protocol settings, such as fees and risk parameters.

Instruction flow includes:

- Trading instructions like place_perp_order for opening positions.

- Risk management instructions, such as liquidate, for handling insolvent accounts.

- Liquidity mechanisms, potentially via keepers, ensuring JIT execution.

At the core is the User Account/Subaccount, which serves as the primary interface for each user, holding their deposited collateral, open trading positions, and accumulated profit and loss (P&L). Users have the capability to manage multiple subaccounts under a single primary account, allowing for the segregation of trading strategies or risk management. The protocol also utilizes Vault Accounts, which refer to the program and vault addresses within the Drift ecosystem, crucial for identifying and interacting with the protocol on the Solana blockchain. The mainnet instance of Drift Protocol operates with the Program Address dRiftyHA39MWEi3m9aunc5MzRF1JYuBsbn6VPcn33UH and the Vault Address JCNCMFXo5M5qwUPg2Utu1u6YWp3MbygxqBsBeXXJfrw.

For its lending and borrowing markets, Drift employs dedicated Lend/Borrow Accounts to track user deposits intended for lending and the outstanding amounts borrowed by users. To enhance the protocol’s resilience, the Insurance Fund Account holds assets staked by users, which generate yield from exchange fees and are intended to cover potential losses that may occur within the protocol. Liquidity provision is facilitated through Backstop AMM Liquidity (BAL) Accounts, which are utilized by liquidity providers who contribute to the Backstop AMM with leveraged positions to earn yield. The protocol’s operational aspects are managed through accounts such as the Fee Pool Account, which accumulates trading fees generated by the platform , and the P&L Pool Account, which is associated with the profits and losses resulting from users’ trading activities. Drift also supports Delegated Accounts, a feature that allows a user to grant another Solana account limited permissions to act on their behalf, specifically for actions such as depositing funds and placing or canceling orders.

The trading engine relies on Perpetual Market Accounts and Spot Market Accounts, which store the state of each respective market, including details like AMM reserves, funding rates (for perpetual markets), open interest, and token balances along with borrow/lend rates (for spot markets). Accurate and real-time pricing is ensured through Oracle Accounts, which hold the price feeds for each trading market, primarily sourced from the Pyth Network. This intricate network of on-chain accounts allows Drift Protocol to manage its diverse functionalities in a modular and transparent manner, with clear segregation of user funds, trading operations, and protocol-level functions. The introduction of delegated accounts further enhances the platform’s flexibility, enabling more sophisticated trading strategies and potential integrations.

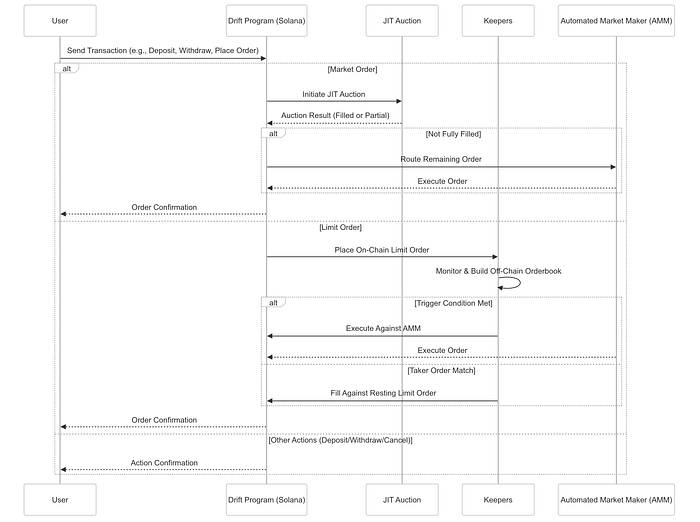

Flow of instructions in Drift

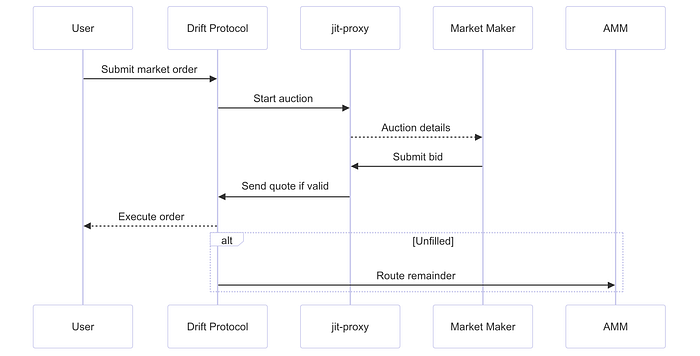

The Drift Protocol orchestrates its instruction flow by enabling users to initiate interactions through transactions sent to its designated program address on the Solana blockchain. These transactions invoke specific program instructions tied to user actions, such as depositing or withdrawing assets, placing trading orders, or canceling existing ones. Market orders, in particular, kick off with a Just-In-Time (JIT) auction to optimize execution.

Meanwhile, a network of Keepers monitors on-chain limit orders, building an off-chain orderbook and playing a pivotal role in matching taker orders with resting limit orders or routing them to the Automated Market Maker (AMM) when triggered.

The AMM acts as a reliable backstop, guaranteeing liquidity for market orders unmatched during the JIT auction or by limit orders.

Running in parallel, the risk engine continuously assesses users’ margin requirements — based on collateral and open positions — initiating liquidations if needed to safeguard the protocol’s solvency. This sophisticated, multi-layered design seamlessly blends on-chain order placement with off-chain orderbook management, delivering enhanced performance and a streamlined user experience. The diagram below illustrates this user flow.

Deep Dive into the Perpetuals Engine

Drift Protocol’s perpetuals engine enables users to engage in leveraged trading on a variety of crypto assets without the constraints of expiration dates, providing a continuous trading experience.

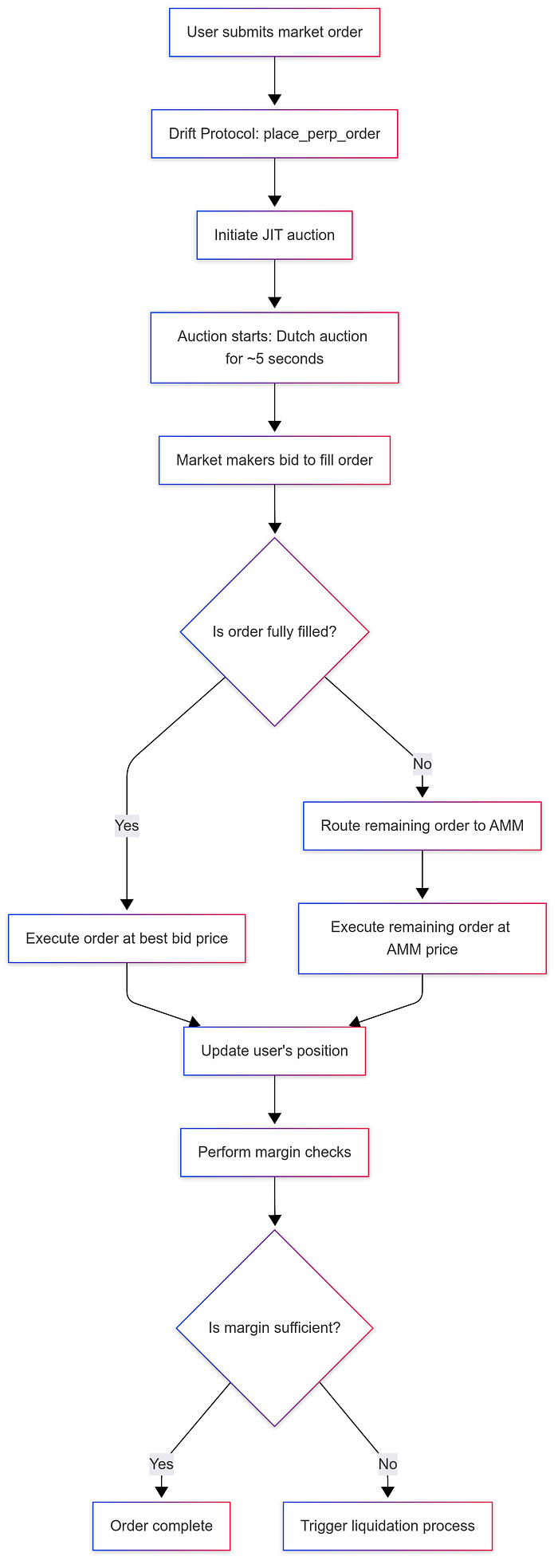

When traders place orders via the place_perp_order instruction, the engine performs margin requirement checks, validates market conditions, and either matches the order immediately with JIT or stores it in the order book for later execution.

The hybrid approach adopted by Drift, combining a traditional orderbook model with the potential for JIT liquidity, suggests a sophisticated order matching system. This system likely prioritizes utilizing existing orderbook depth but can also strategically tap into JIT liquidity to achieve better pricing and higher fill rates for traders, particularly for larger orders that might otherwise experience significant slippage.

Position Management

Positions within Drift’s perpetuals engine are managed with a focus on capital efficiency and risk mitigation. The protocol utilizes a cross-margined risk engine, enabling users to leverage any deposited token as collateral for their perpetual swap positions, as well as for other DeFi functionalities offered by the platform. To provide flexibility and enhanced risk management, each user has a primary account and the option to create multiple subaccounts, allowing for the isolation of different trading strategies or positions. The details of each trading position, including the quantity of the base asset, the corresponding quote asset value, the average entry price, and the current unrealized profit or loss (P&L), are meticulously tracked within the user’s designated account. The risk engine plays a critical role in continuously calculating margin requirements for each user based on factors such as the collateral weight assigned to the deposited assets, the size of the user’s open positions, and the prevailing market volatility. To maintain the alignment of the perpetual swap price with the price of the underlying asset, the protocol implements periodic funding payments between holders of long and short positions. Furthermore, Drift provides users with tools to proactively manage their risk, including the ability to set stop-loss orders to limit potential losses and take-profit orders to automatically close positions at a desired profit level. This comprehensive system for position management emphasizes both capital efficiency through cross-margining and robust risk control through various features and automated mechanisms.

The core logic for handling trade execution and managing user positions is likely housed within the programs/clearing_house/src/lib.rs file of the protocol-v2 repository. The implementation of the Automated Market Maker, which plays a crucial role in providing liquidity and determining execution prices, would be detailed in the programs/amm/src/lib.rs file. The functionality of the decentralized limit order book and its interaction with the network of Keeper Bots would be found in the programs/orderbook/src/lib.rs file. For developers looking to integrate with the Just-In-Time liquidity mechanism, the sdk/src/jitProxyClient.ts file within the protocol-v2 repository provides the necessary Typescript SDK.

Unpacking the Risk Engine

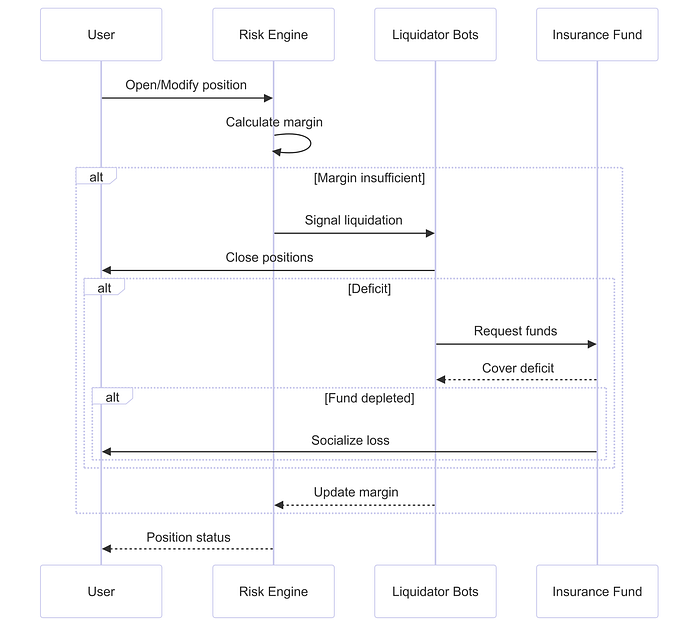

Drift Protocol’s risk engine ensures stability by enforcing margin requirements using a cross-margined system, where all user collateral supports their positions for greater efficiency. It assigns collateral weights — lower for volatile assets — and adjusts for concentration risk or liabilities. Initial and maintenance margin ratios guide position opening and liquidation thresholds, with safeguards like price bands preventing risky trades during volatility. If a user’s margin ratio drops below maintenance, Liquidator Bots, incentivized by rewards, close positions. An Insurance Fund covers deficits, with socialized loss as a fallback. Liquidation shields mitigate rapid price drops.

To accurately assess risk, the protocol assigns a collateral weight to each supported asset, which dictates the percentage of the asset’s value that can contribute to a user’s margin. More volatile assets may have lower collateral weights, reflecting their higher risk profile. Additionally, to mitigate concentration risk, the protocol may discount the collateral weight of assets held in very large quantities by a single user. Conversely, liabilities, such as borrowed funds or open perpetual swap positions, may have premiums applied to their margin requirements, increasing the amount of collateral needed to support them. Drift distinguishes between the initial margin ratio, which is the minimum collateral required to open a new trading position, and the maintenance margin ratio, which is the minimum collateral required to keep a position open. The maintenance margin is typically lower than the initial margin, acting as a threshold for potential liquidation. The risk engine also incorporates safeguards against market volatility and manipulation, such as price bands that restrict order placement if the oracle price and the mark price diverge significantly, and mechanisms to prevent risk-increasing trades during periods of high price volatility. These parameters and calculations collectively form a robust framework for managing risk within the Drift Protocol ecosystem.

When a user’s margin ratio, calculated as the ratio of their collateral to the total value of their open positions and borrows, falls below the maintenance margin requirement, the protocol initiates the process of liquidation. This is a crucial mechanism to prevent undercollateralized positions from leading to losses that could impact other users or the protocol’s insurance fund. Drift employs a decentralized network of Liquidator Bots that continuously monitor user accounts for those that fall below the required collateral levels. These bots are incentivized to perform liquidations by receiving a reward, typically a percentage of the liquidated amount. The primary goal of liquidation is to bring the user’s margin ratio back above the maintenance margin level, usually by closing out a portion or all of their open positions. In situations where a user’s losses exceed their collateral, and they become bankrupt, Drift utilizes its Insurance Fund to cover the deficit. If, in extreme circumstances, the Insurance Fund is insufficient to cover all losses, the protocol may implement a system of socialized loss, where the remaining losses are distributed among other market participants. To mitigate the risks associated with rapid price drops, Drift has implemented liquidation shields, such as flash crash protection and oracle price deviation limits, which aim to slow down the liquidation process during sudden market movements. This multi-faceted approach to risk management, involving dynamic margin calculations, incentivized liquidations, and a safety net provided by the Insurance Fund, is central to the operational integrity of Drift Protocol.

The core logic for calculating margin requirements and determining liquidation eligibility is likely implemented in the programs/risk_engine/src/lib.rs file within the protocol-v2 repository. The process of triggering and executing liquidations would likely be handled by code within the programs/clearing_house/src/lib.rs file. Developers interested in building their own liquidation bots can utilize the Typescript SDK provided in the sdk/src/liquidatorClient.ts file of the protocol-v2 repository.

Exploring Just-In-Time (JIT) Liquidity

The Just-In-Time (JIT) liquidity mechanism is a core innovation within Drift Protocol, designed to enhance liquidity, particularly for market orders in both spot and perpetuals trading, effectively addressing the inherent limitations of on-chain liquidity pools. When a user submits a market order, the protocol instantly initiates a short-term Dutch auction, typically lasting around five seconds. During this brief window, market makers, acting as liquidity providers, have the opportunity to bid on the order, aiming to fill it at a price that is equal to or better than the auction price. This competitive bidding process is crucial for achieving optimal execution prices for traders.

The pricing within the JIT auction follows a predefined structure. For buy orders, the auction price starts at the Automated Market Maker’s (AMM) bid price and linearly progresses towards the AMM’s intrinsic price. Conversely, for sell orders, the price starts at the AMM’s ask price and moves towards the AMM’s intrinsic price. This Dutch auction format incentivizes market makers to submit their most competitive quotes early in the auction period to increase their chances of filling the order. Market makers compete based on the speed of their submissions to capture the opportunity to provide liquidity.

If the market order is not fully filled by the participating market makers during the JIT auction timeframe, the remaining portion of the order is then routed to the backstop AMM for execution at the estimated entry price. This ensures that all market orders are ultimately filled, either by active market makers or by the protocol’s internal AMM. The JIT liquidity mechanism represents a significant advancement in on-chain exchange design, aiming to provide the benefits of a request-for-quote (RFQ) system within a decentralized framework, supplemented by the guaranteed liquidity of an AMM.

To facilitate the participation of market makers in the JIT liquidity mechanism, Drift Protocol utilizes the jit-proxy program, which is an open-source, permissionless, and stateless program deployed on the Solana blockchain. The primary role of the jit-proxy is to simplify the process for market makers to offer JIT liquidity on Drift v2. This program allows market makers to automatically create and submit Drift perpetual and spot orders during the JIT auction based on their pre-configured market preferences and maximum position sizes. It performs crucial on-chain checks at the last moment to ensure that the proposed fill price aligns with the market maker's desired bid or ask price and that the resulting position does not exceed their established limits. The jit-proxy program interacts with the main Drift Protocol (protocol-v2) by listening for incoming market orders and subsequently submitting the market maker's quotes during the auction window. This communication is facilitated by Solana's inter-program communication capabilities. To enable developers to build and integrate with the jit-proxy, Drift provides SDKs in both Typescript (within the protocol-v2 repository) and Python (within the jit-proxy repository). These SDKs offer the necessary tools and abstractions for market makers to easily interact with the jit-proxy program and participate in the JIT liquidity mechanism. The stateless and permissionless nature of the jit-proxy encourages broad participation from market makers, ultimately contributing to enhanced liquidity and better execution prices for all users of Drift Protocol.

The src/lib.rs file within the jit-proxy repository likely contains the core logic of the JIT proxy program, detailing how it processes incoming instructions related to taker orders and how it facilitates the submission of maker quotes based on predefined parameters. The ts/sdk/Readme.md file in the jit-proxy repository serves as a guide for developers, providing documentation and illustrative examples on how to utilize the Typescript SDK to interact with the JIT proxy program effectively.

Unique Flavour Of Drift

Drift Protocol incorporates several innovative implementation details that contribute to its unique position within the decentralized finance landscape. One of the most notable is its hybrid liquidity model, which strategically blends the benefits of Just-In-Time (JIT) auctions, a Decentralized Limit Order Book (DLOB), and an Automated Market Maker (AMM). This combination allows Drift to offer deep liquidity, tight trading spreads, and efficient order execution across various market conditions and order types, potentially surpassing the capabilities of DEXs that rely on a singular liquidity mechanism.

Another key innovation is the Decentralized Limit Order Book (DLOB) managed by Keeper Bots with economic incentives. By utilizing an off-chain orderbook structure maintained by a network of incentivized Keepers, Drift achieves the functionality of a traditional orderbook without incurring the significant computational overhead associated with a fully on-chain central limit order book (CLOB). The economic incentives provided to Keepers ensure their active participation in monitoring, sorting, and filling orders, contributing to a liquid and responsive orderbook experience on a high-throughput blockchain like Solana.

Drift’s cross-margined risk engine is another significant innovation, enhancing capital efficiency for users by allowing them to use a diverse range of deposited assets as collateral across all their trading positions. This approach contrasts with isolated margin systems, where each trading pair requires its own dedicated collateral, often leading to underutilized capital. The cross-margined system in Drift enables traders to manage their risk and capital more effectively across their entire portfolio.

Furthermore, Drift’s expansion beyond core perpetuals trading to include prediction markets (BET) and automated Market Maker Vaults showcases its commitment to innovation and to catering to a broader spectrum of users. The integration of prediction markets adds a unique dimension to the platform, while the Market Maker Vaults democratize access to sophisticated liquidity provision strategies.

A particularly noteworthy implementation detail could be the specific algorithms employed by Drift’s AMM to dynamically adjust its peg and trading spreads. As indicated in the documentation, these adjustments are based on real-time oracle prices, market volatility, and the AMM’s inventory skew. This dynamic nature of the AMM aims to optimize its performance, maintain price accuracy relative to external markets, and enhance its resilience to market fluctuations. Examining the source code within the programs/amm/src/lib.rs directory (if accessible) would provide valuable insights into the precise mathematical formulas and underlying logic governing these adaptive AMM parameters.

References